9,883+% Returns in 3 years on Cryptocurrency using 2D Convolutional Neural Network (CNN) Model and short listing Best Assets for Trading — VishvaAlgo Machine Learning Trading Bot

Unleashing the power of Neural Networks for creating Trading Bot for maximum profits.

Introduction:

Welcome to the world of algorithmic trading and machine learning, where innovation meets profitability. Over the past three years, I’ve dedicated myself to developing algorithmic trading systems that harness the power of various strategies. Through relentless experimentation and refinement, I’ve achieved impressive returns across multiple strategies, delighting members of my Patreon community with consistent profits.

In the pursuit of excellence, I recently launched VishvaAlgo, a machine learning-based algorithmic trading system that leverages neural network classification models. This cutting-edge platform has already demonstrated remarkable results, delivering exceptional returns to traders in the cryptocurrency market. Through a series of articles and practical demonstrations, I’ve shared insights on transitioning from traditional algorithmic trading to deploying practical machine learning models, showcasing their effectiveness in real-world trading environments.

In this article, we delve into the trans-formative potential of algorithmic trading and machine learning, focusing on the effectiveness of neural networks, specifically the Convolutional neural networks (CNNs) models. Building upon our past successes, we set out to demonstrate the remarkable profitability achievable with advanced machine learning models, using Bitcoin (BTC) and Ethereum (ETH) as our primary assets.

Our analysis focuses on Ethereum pricing in USDT, utilizing 15-minute candlestick data spanning from January 1st, 2021, to October 22nd, 2023, comprising over 97,000 rows of data and more than 190 features. By leveraging neural network models for prediction, we aim to identify optimal long and short positions, showcasing the potential of deep learning in financial markets.

Our story is one of relentless innovation, fueled by a burning desire to unlock the full potential of Deep Learning in the pursuit of profit. In this article, we invite you to join us as we unravel the exciting tale of our transformation from humble beginnings to groundbreaking success.

Our Algorithmic Trading Vs/+ Machine Learning Vs/+ Deep Learning Journey so far?

Stage 1:

We have developed a crypto Algorithmic Strategy which gave us huge profits when ran on multiple crypto assets (138+) with a profit range of 8787%+ in span of 3 years (almost).

“The 8787%+ ROI Algo Strategy Unveiled for Crypto Futures! Revolutionized With Famous RSI, MACD, Bollinger Bands, ADX, EMA” — Link

We have run live trading in dry-run mode for the same for 7 days and details about the same have been shared in another article.

“Freqtrade Revealed: 7-Day Journey in Algorithmic Trading for Crypto Futures Market” — Link

After successful backtest results and forward testing (live trading in dry-run mode), we planned to improve the odds of making more profit for the same. (To lower stop-losses, increase odds of winning more , reduce risk factor and other important things)

Stage 2:

We have worked on developing a strategy alone without freqtrade setup (avoiding trailing stop loss, multiple asst parallel running, higher risk management setups that freqtrade provides for free (it is a free open source platform) and then tested it in market, then optimized it using hyper parameters and then , we got some +ve profits from the strategy

“How I achieved 3000+% Profit in Backtesting for Various Algorithmic Trading Bots and how you can do the same for your Trading Strategies — Using Python Code” — Link

Stage 3:

As we have tested our strategy only on 1 Asset , i.e; BTC/USDT in crypto market, we wanted to know if we can segregate the whole collective assets we have (Which we have used for developing Freqtrade Strategy earlier) segregate them into different clusters based on their volatility, it becomes easy to do trading for certain volatile assets and won’t hit huge stop-losses for others if worked on implementing based on coin volatility.

We used K-nearest Neighbors (KNN Means) to identify different clusters of assets out of 138 crypto assets we use in our freqtrade strategy, which gave us 8000+% profits during backtest.

“Hyper Optimized Algorithmic Strategy Vs/+ Machine Learning Models Part -1 (K-Nearest Neighbors)” — Link

Stage 4:

Now, we want to introduce Unsupervised Machine Learning model — Hidden Markov Model (HMMs) to identify trends in the market and trade during only profitable trends and avoid sudden pumps, dumps in market, avoid negative trends in market. Below explanation unravels the same.

“Hyper Optimized Algorithmic Strategy Vs/+ Machine Learning Models Part -2 (Hidden Markov Model — HMM)” — Link

Stage 5:

I worked on using XGBoost Classifier to identify long and short trades using our old signal. Before using it, we ensured that the signal algorithm we had previously developed was hyper-optimized. Additionally, we introduced different stop-loss and take-profit parameters for this setup, causing the target values to change accordingly. We also adjusted the parameters used for obtaining profitable trades based on the stop-loss and take-profit values. Later, we tested the basic XGBClassifier setup and then enhanced the results by adding re-sampling methods. Our target classes, which include 0’s (neutral), 1’s (for long trades), and 2’s (for short trades), were imbalanced due to the trade execution timing. To address this imbalance, we employed re-sampling methods and performed hyper-optimization of the classifier model. Subsequently, we evaluated if the model performed better with other classifier models such as SVC, CatBoost, and LightGBM, in combination with LSTM and XGBoost. Finally, we concluded by analyzing the results and determining feature importance parameters to identify the most productive features.

“Hyper Optimized Algorithmic Strategy Vs/+ Machine Learning Models Part -3 (XGBoost Classifier , LGBM Classifier, CatBoost Classifier, SVC, LSTM with XGB and Multi level Hyper-optimization)” — Link

Stage 6:

In that stage, I utilized the CatBoostClassifier along with resampling and sample weights. I incorporated multiple time frame indicators such as volume, momentum, trend, and volatility into my model. After running the model, I performed ensembling techniques to enhance its overall performance. The results of my analysis showed a significant increase in profit from 54% to over 4600% during backtesting. Additionally, I highlighted the impressive performance metrics including recall, precision, accuracy, and F1 score, all exceeding 80% for each of the three trading classes (0 for neutral, 1 for long, and 2 for short trades).

“From 54% to a Staggering 4648%: Catapulting Cryptocurrency Trading with CatBoost Classifier, Machine Learning Model at Its Best” — Link

Stage 7:

In this stage, the ensemble method combining TCN and LSTM neural network models has demonstrated exceptional performance across various datasets, outperforming individual models and even surpassing buy and hold strategies. This underscores the effectiveness of ensemble learning in improving prediction accuracy and robustness.

“Bitcoin/BTC 4750%+ , Etherium/ETH 11,270%+ profit in 1023 days using Neural Networks, Algorithmic Trading Vs/+ Machine Learning Models Vs/+ Deep Learning Model Part — 4 (TCN, LSTM, Transformer with Ensemble Method)” — Link

Stage 8:

Experience the future of trading with VishvaAlgo v3.8. With its advanced features, unparalleled risk management capabilities, and ease of integration of ML and neural network models, VishvaAlgo is the ultimate choice for traders seeking consistent profits and peace of mind. Don’t miss out on this opportunity to revolutionize your trading journey.

Purchase Link: VishvaAlgo V3.8 Live Crypto Trading Using Machine Learning Model

“VishvaAlgo v3.0 — Revolutionize Your Live Cryptocurrency Trading system Enhanced with Machine Learning (Neural Network) Model. Live Profits Screenshots Shared” — Link

Youtube Link Explanation of VishvaAlgo v4.x Features — Link

get entire code and profitable algos @ https://patreon.com/pppicasso

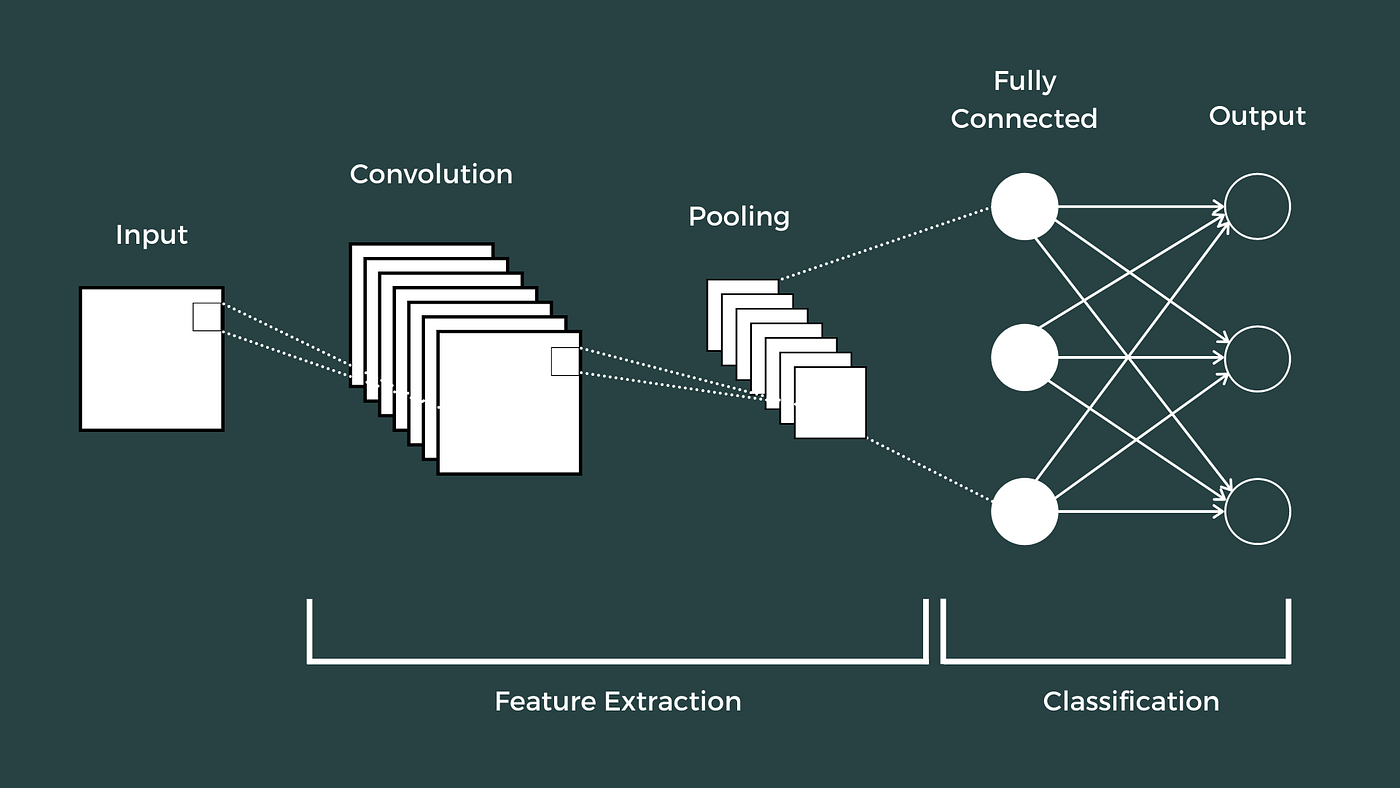

Introduction to CNNs and Time Series Classification

Convolutional Neural Networks (CNNs) are primarily designed for processing grid-like data, such as images and videos, where they have proven highly effective. CNNs work by applying convolutional filters that scan the input data and learn spatial hierarchies of features. Typically used in image and video processing, CNNs can also be adapted for time series data due to their ability to capture local patterns and trends.

CNNs for Image and Video Processing

- Image Processing: CNNs are used to identify objects, detect faces, and recognize patterns within images. They work by applying a series of convolutional layers, pooling layers, and fully connected layers to extract features and make predictions.

- Video Processing: In video data, CNNs can be used for tasks like action recognition and video classification. They process each frame as an image and can use temporal layers to capture the sequence of frames.

CNNs for Time Series Data

Despite their typical use in image and video processing, CNNs can be highly effective for time series classification. Here’s how:

- Feature Extraction: CNNs can extract temporal features from time series data, identifying patterns such as trends, seasonality, and anomalies.

- Local Pattern Recognition: The convolutional filters can capture local patterns within the time series data, which is crucial for financial data where short-term trends and fluctuations matter.

- Dimensionality Reduction: Pooling layers can reduce the dimensionality of the data, retaining the most important features while reducing computational complexity.

2D CNN for Multi-Class Classification on ETH Data

Data Description

- Asset: Ethereum (ETH)

- Time Frame: 15-minute intervals

- Rows: Over 100,000

- Features: 193+ (e.g., OHLCV, technical indicators)

Model Architecture and Training

- Input Shape: The input data for the model is structured in a 2D format, with the shape (number of samples, number of timesteps, number of features).

- Convolutional Layers: These layers apply convolutional filters across the input data to learn local temporal features.

x = Conv2D(filters=64, kernel_size=(3, 3), activation='relu')(inputs)

3. Pooling Layers: These layers reduce the dimensionality of the feature maps while retaining important information.

x = MaxPooling2D(pool_size=(2, 2))(x)

4. Dense Layers: Fully connected layers interpret the features extracted by the convolutional layers.

x = Flatten()(x) x = Dense(units=128, activation='relu')(x)

5. Output Layer: The final layer uses a softmax activation function to output probabilities for each class (neutral, long, short).

outputs = Dense(3, activation='softmax')(x)

Training the Model

The model is trained using labeled time series data, where each segment of the time series is labeled as 0 (neutral), 1 (long), or 2 (short).

model.compile(optimizer='adam', loss='categorical_crossentropy', metrics=['accuracy'])

model.fit(X_train, y_train, epochs=50, batch_size=64, validation_split=0.2)Example Code

Here is a complete example of a 2D CNN for multi-class classification of ETH time series data:

import numpy as np

import keras

from keras.models import Model

from keras.layers import Input, Conv2D, MaxPooling2D, Flatten, Dense, Dropout

from keras.utils import to_categorical

from sklearn.model_selection import train_test_split

# Simulate data

X = np.random.rand(100000, 15, 193, 1) # 100,000 samples, 15 timesteps, 193 features, 1 channel

y = np.random.randint(3, size=100000) # 100,000 labels (0, 1, 2)

# Convert labels to one-hot encoding

y = to_categorical(y, num_classes=3)

# Split data into training and validation sets

X_train, X_val, y_train, y_val = train_test_split(X, y, test_size=0.2, random_state=42)

# Build model

inputs = Input(shape=(15, 193, 1))

x = Conv2D(filters=64, kernel_size=(3, 3), activation='relu')(inputs)

x = MaxPooling2D(pool_size=(2, 2))(x)

x = Flatten()(x)

x = Dense(units=128, activation='relu')(x)

x = Dropout(0.5)(x)

outputs = Dense(3, activation='softmax')(x)

model = Model(inputs=inputs, outputs=outputs)

model.compile(optimizer='adam', loss='categorical_crossentropy', metrics=['accuracy'])

# Train model

model.fit(X_train, y_train, epochs=10, batch_size=64, validation_data=(X_val, y_val))Effectiveness of CNNs for Time Series Classification

- Pattern Recognition: CNNs can effectively capture and recognize patterns in time series data, making them suitable for financial market analysis.

- Speed: CNNs can process large datasets efficiently, which is crucial for high-frequency trading strategies.

- Accuracy: When properly tuned, CNNs can achieve high accuracy in predicting market movements, helping traders make informed decisions.

In summary, while CNNs are traditionally used for image and video processing, their ability to capture local patterns and reduce dimensionality makes them highly effective for time series classification in financial markets. This adaptability allows for robust models that can predict market movements, such as those in the cryptocurrency market, aiding in the classification of positions like long, short, and neutral.

The Whole code Explanation:

Youtube Link Explanation of VishvaAlgo v4.x Features — Link

get entire code and profitable algos @ https://patreon.com/pppicasso

# Remove Future Warnings

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

# Suppress PerformanceWarning

warnings.filterwarnings("ignore")

# General

import numpy as np

# Data Management

import pandas as pd

# Machine Learning

from catboost import CatBoostClassifier

from sklearn.model_selection import train_test_split

from sklearn.model_selection import RandomizedSearchCV, cross_val_score

from sklearn.model_selection import RepeatedStratifiedKFold

from sklearn.linear_model import LogisticRegression

# ensemble

from sklearn.ensemble import RandomForestClassifier, GradientBoostingClassifier

from sklearn.ensemble import StackingClassifier

from sklearn.ensemble import VotingClassifier

#Sampling Methods

from imblearn.over_sampling import ADASYN

#Scaling

from sklearn.preprocessing import MinMaxScaler

# Binary Classification Specific Metrics

from sklearn.metrics import RocCurveDisplay as plot_roc_curve

# General Metrics

from sklearn.metrics import accuracy_score

from sklearn.metrics import precision_score

from sklearn.metrics import confusion_matrix, classification_report, roc_curve, roc_auc_score, accuracy_score

from sklearn.metrics import precision_score

from sklearn.metrics import ConfusionMatrixDisplay

# Reporting

import matplotlib.pyplot as plt

from matplotlib.pylab import rcParams

from xgboost import plot_tree

#Backtesting

from backtesting import Backtest

from backtesting import Strategy

#hyperopt

from hyperopt import fmin, tpe, hp

from pandas_datareader.data import DataReader

import json

from datetime import datetime

import talib as ta

import ccxt

# from sklearn.model_selection import train_test_split

from sklearn.utils import class_weight

from keras.models import Sequential

from keras.layers import LSTM, Dense, Dropout

from keras.optimizers import Adam

# from keras.wrappers.scikit_learn import KerasClassifier

from sklearn.ensemble import VotingClassifier

from hyperopt import fmin, tpe, hp, STATUS_OK, TrialsImport Statements (Lines 1–18):

- Warnings (Lines 1–4):

- These lines suppress warnings that might appear during execution. While this can be helpful for uninterrupted training, it’s generally recommended to address the warnings themselves for better debugging and understanding potential issues.

- General Libraries (Lines 5–7):

numpy (np): Provides numerical computing capabilities, often used for array operations and mathematical functions. Not directly applicable to article writing.pandas (pd): Used for data manipulation, analysis, and visualization. Essential for working with structured data in articles (e.g., tables, charts).- Machine Learning Libraries (Lines 8–13):

catboost(not explicitly imported here): Provides a powerful gradient boosting library for machine learning tasks. Not directly relevant to article writing unless you're discussing specific machine learning algorithms.scikit-learn(various submodules): A comprehensive machine learning library. Parts might be useful for illustrating concepts or comparing approaches in articles:train_test_split: Splits data into training and testing sets for model evaluation.RandomizedSearchCV,cross_val_score,RepeatedStratifiedKFold: Techniques for hyperparameter tuning and model evaluation (cross-validation).LogisticRegression: A linear classification model. Potentially relevant if discussing classification algorithms.- Ensemble Methods (Lines 14–16):

scikit-learn(submodules): Techniques for combining multiple models to improve performance. Not directly applicable to article writing.- Sampling Methods (Line 17):

imblearn: Provides tools for handling imbalanced datasets (where classes have unequal sizes). Not typically used in article writing itself.- Scaling (Line 18):

scikit-learn: Techniques for normalizing or standardizing data (often necessary for machine learning models). Can be relevant in articles to explain data preprocessing steps.

Metrics (Lines 19–33):

- Binary Classification Metrics (Lines 19–21):

scikit-learn: Used to evaluate the performance of classification models, particularly for binary classification (two classes). Not directly applicable to article writing unless discussing model evaluation metrics.- General Metrics (Lines 22–33):

scikit-learn: Various metrics for evaluating model performance across different classification tasks. Can be useful in articles to explain how models are assessed:accuracy_score: Proportion of correct predictions.precision_score: Proportion of true positives among predicted positives.confusion_matrix: Visualization of how many instances were classified correctly or incorrectly for each class.classification_report: Detailed report on model performance, including precision, recall, F1-score, and support for each class.roc_curve,roc_auc_score: Measures for assessing the Receiver Operating Characteristic (ROC) curve, which helps evaluate a model's ability to discriminate between classes.

Reporting (Lines 34–36):

matplotlib.pyplot (plt): Used for creating visualizations like charts and graphs. Essential for presenting data and model results in articles.

Backtesting (Lines 37–38):

backtesting: Library for backtesting trading strategies. Not relevant to article writing unless discussing financial applications of machine learning.

Hyperparameter Optimization (Lines 39–42):

hyperopt: Library for hyperparameter tuning (finding the best settings for machine learning models). Not directly applicable to article writing.

Data Retrieval (Line 43):

pandas_datareader: Facilitates data retrieval from various financial data sources. Not typically used in article writing itself.

Other Imports (Lines 44–50):

json: For working with JSON data format (not directly used here).datetime: For working with date and time objects. Can be useful in articles for handling time-series data.talib: Technical analysis library for financial markets (not directly used here).ccxt(not explicitly imported here): Library for interacting with cryptocurrency exchanges (not relevant to article writing).

Context:

- Each library and module is imported with a specific purpose, such as data manipulation, machine learning, evaluation, visualization, backtesting, hyperparameter optimization, etc.

- These libraries and modules will be used throughout the code for various tasks like data preprocessing, model training, evaluation, optimization, and visualization.

# Define the path to your JSON file

file_path = './ETH_USDT_USDT-15m-futures.json'

# Open the file and read the data

with open(file_path, "r") as f:

data = json.load(f)

df = pd.DataFrame(data)

# Extract the OHLC data (adjust column names as needed)

# ohlc_data = df[["date","open", "high", "low", "close", "volume"]]

df.rename(columns={0: "Date", 1: "Open", 2: "High",3: "Low", 4: "Adj Close", 5: "Volume"}, inplace=True)

# Convert timestamps to datetime objects

df["Date"] = pd.to_datetime(df['Date'] / 1000, unit='s')

df.set_index("Date", inplace=True)

# Format the date index

df.index = df.index.strftime("%m-%d-%Y %H:%M")

df['Close'] = df['Adj Close']

# print(df.dropna(), df.describe(), df.info())

data = df

dataTo analyze historical cryptocurrency futures data, we can first load the data from a JSON file. The provided code demonstrates how to use Python’s json library to parse the JSON content into a dictionary. We then convert this dictionary into a pandas DataFrame for easier manipulation. The DataFrame is cleaned and transformed by renaming columns, converting timestamps to datetime objects, setting the date as the index, and formatting the date display for better readability.

Here’s the step-by-step explanation of the code:

1. Loading JSON Data:

- The code defines a file path (

file_path) to a JSON file containing cryptocurrency data (presumably in the format of Open-High-Low-Close-Volume for Ethereum futures contracts traded with USDT). - It opens the file for reading (

with open(file_path, "r") as f:) and usesjson.load(f)to parse the JSON content into a Python dictionary (data).

2. Converting to DataFrame:

- The code creates a pandas DataFrame (

df) from the loaded dictionary (data). A DataFrame is a tabular data structure similar to a spreadsheet, making it easier to work with and analyze the data.

3. Data Cleaning and Transformation:

- This part assumes the JSON data has columns with numerical indices (0, 1, 2, etc.) instead of meaningful names. It renames these columns to more descriptive labels (

"Date","Open","High","Low","Adj Close","Volume") usingdf.rename(columns={...}, inplace=True). - It converts the

"Date"column from timestamps (likely in milliseconds since some epoch) to datetime objects usingpd.to_datetime(). This makes it easier to work with dates and perform time-based operations. - The code sets the

"Date"column as the index of the DataFrame usingdf.set_index("Date", inplace=True). This allows you to efficiently access and filter data based on dates. - It formats the date index using

df.index.strftime("%m-%d-%Y %H:%M")to display dates in a more readable format (e.g., "05-14-2024 16:35"). - Finally, it assigns the column named

"Adj Close"(assuming it represents the adjusted closing price) to a variable named"Close"for potentially clearer reference.

# Assuming you have a DataFrame named 'df' with columns 'Open', 'High', 'Low', 'Close', 'Adj Close', and 'Volume'

target_prediction_number = 2

time_periods = [6, 8, 10, 12, 14, 16, 18, 22, 26, 33, 44, 55]

name_periods = [6, 8, 10, 12, 14, 16, 18, 22, 26, 33, 44, 55]

df = data.copy()

new_columns = []

for period in time_periods:

for nperiod in name_periods:

df[f'ATR_{period}'] = ta.ATR(df['High'], df['Low'], df['Close'], timeperiod=period)

df[f'EMA_{period}'] = ta.EMA(df['Close'], timeperiod=period*2)

df[f'RSI_{period}'] = ta.RSI(df['Close'], timeperiod=period*0.5)

df[f'VWAP_{period}'] = ta.SUM(df['Volume'] * (df['High'] + df['Low'] + df['Close']) / 3, timeperiod=period) / ta.SUM(df['Volume'], timeperiod=period)

df[f'ROC_{period}'] = ta.ROC(df['Close'], timeperiod=period)

df[f'KC_upper_{period}'] = ta.EMA(df['High'], timeperiod=period*2)

df[f'KC_middle_{period}'] = ta.EMA(df['Low'], timeperiod=period*2)

df[f'Donchian_upper_{period}'] = ta.MAX(df['High'], timeperiod=period)

df[f'Donchian_lower_{period}'] = ta.MIN(df['Low'], timeperiod=period)

macd, macd_signal, _ = ta.MACD(df['Close'], fastperiod=(period + 12), slowperiod=(period + 26), signalperiod=(period + 9))

df[f'MACD_{period}'] = macd

df[f'MACD_signal_{period}'] = macd_signal

bb_upper, bb_middle, bb_lower = ta.BBANDS(df['Close'], timeperiod=period*0.5, nbdevup=2, nbdevdn=2)

df[f'BB_upper_{period}'] = bb_upper

df[f'BB_middle_{period}'] = bb_middle

df[f'BB_lower_{period}'] = bb_lower

df[f'EWO_{period}'] = ta.SMA(df['Close'], timeperiod=(period+5)) - ta.SMA(df['Close'], timeperiod=(period+35))

df["Returns"] = (df["Adj Close"] / df["Adj Close"].shift(target_prediction_number)) - 1

df["Range"] = (df["High"] / df["Low"]) - 1

df["Volatility"] = df['Returns'].rolling(window=target_prediction_number).std()

# Volume-Based Indicators

df['OBV'] = ta.OBV(df['Close'], df['Volume'])

df['ADL'] = ta.AD(df['High'], df['Low'], df['Close'], df['Volume'])

# Momentum-Based Indicators

df['Stoch_Oscillator'] = ta.STOCH(df['High'], df['Low'], df['Close'])[0]

# Calculate the Elliott Wave Oscillator (EWO)

#df['EWO'] = ta.SMA(df['Close'], timeperiod=5) - ta.SMA(df['Close'], timeperiod=35)

# Volatility-Based Indicators

# df['ATR'] = ta.ATR(df['High'], df['Low'], df['Close'], timeperiod=14)

# df['BB_upper'], df['BB_middle'], df['BB_lower'] = ta.BBANDS(df['Close'], timeperiod=20, nbdevup=2, nbdevdn=2)

# df['KC_upper'], df['KC_middle'] = ta.EMA(df['High'], timeperiod=20), ta.EMA(df['Low'], timeperiod=20)

# df['Donchian_upper'], df['Donchian_lower'] = ta.MAX(df['High'], timeperiod=20), ta.MIN(df['Low'], timeperiod=20)

# Trend-Based Indicators

# df['MA'] = ta.SMA(df['Close'], timeperiod=20)

# df['EMA'] = ta.EMA(df['Close'], timeperiod=20)

df['PSAR'] = ta.SAR(df['High'], df['Low'], acceleration=0.02, maximum=0.2)

# Set pandas option to display all columns

pd.set_option('display.max_columns', None)

# Displaying the calculated indicators

print(df.tail())

df.dropna(inplace=True)

print("Length: ", len(df))

dfYoutube Link Explanation of VishvaAlgo v4.x Features — Link

get entire code and profitable algos @ https://patreon.com/pppicasso

This code demonstrates the calculation of various technical indicators using the talib library. The code iterates through different time periods to compute indicators like Average True Range (ATR), Exponential Moving Average (EMA), Relative Strength Index (RSI), and several others. Additionally, it calculates features like returns, range, and volatility to potentially use as input features for machine learning models.

1. Technical Indicator Calculations:

- The code iterates through two lists,

time_periodsandname_periods(which seem to have the same values here). This might be a placeholder for using different sets of periods for the indicators in the future. - Within the loops, it calculates numerous technical indicators for each specified time period (

period) usingtalibfunctions: - Average True Range (ATR): Measures market volatility (

df[f'ATR_{period}']). - Exponential Moving Average (EMA): Calculates EMAs with a period twice the loop’s

period(df[f'EMA_{period}']). - Relative Strength Index (RSI): Calculates RSI with a period half the loop’s

period(df[f'RSI_{period}']). - Volume-Weighted Average Price (VWAP): Calculates VWAP for the

period(df[f'VWAP_{period}']). - Rate of Change (ROC): Calculates ROC for the

period(df[f'ROC_{period}']). - Keltner Channels (KC): Calculates upper and middle bands based on EMAs of highs and lows (

df[f'KC_upper_{period}'],df[f'KC_middle_{period}']). - Donchian Channels: Calculates upper and lower bands based on maximum and minimum highs/lows within the

period(df[f'Donchian_upper_{period}'],df[f'Donchian_lower_{period}']). - Moving Average Convergence Divergence (MACD): Calculates MACD and its signal line for the

period(df[f'MACD_{period}'],df[f'MACD_signal_{period}']). - Bollinger Bands (BB): Calculates upper, middle, and lower bands for the

period(df[f'BB_upper_{period}'],df[f'BB_middle_{period}'],df[f'BB_lower_{period}']). - Elliott Wave Oscillator (EWO): Calculates EWO for the

period(df[f'EWO_{period}']). - Target Prediction and Feature Engineering:

- The code defines a

target_prediction_number(presumably the number of periods ahead you aim to predict). - It calculates “Returns” as the percentage change in adjusted close prices over the

target_prediction_numberperiods (df["Returns"]). - It calculates “Range” as the difference between high and low prices divided by the low price (

df["Range"]). - It calculates “Volatility” as the rolling standard deviation of returns over the

target_prediction_numberperiods (df["Volatility"]). - Additional Indicators:

- The code calculates On-Balance Volume (OBV) and Accumulation Distribution Line (ADL) using

talibfunctions (df['OBV'],df['ADL']). - It calculates the Stochastic Oscillator using

talib(df['Stoch_Oscillator']). - It calculates the Parabolic Stop and Reversal (PSAR) using

talib(df['PSAR']).

Data- Preprocessing — Setting up “Target” value for estimating future predictive values

# Target flexible way

pipdiff_percentage = 0.01 # 1% (0.01) of the asset's price for TP

SLTPRatio = 2.0 # pipdiff/Ratio gives SL

def mytarget(barsupfront, df1):

length = len(df1)

high = list(df1['High'])

low = list(df1['Low'])

close = list(df1['Close'])

open_ = list(df1['Open']) # Renamed 'open' to 'open_' to avoid conflict with Python's built-in function

trendcat = [None] * length

for line in range(0, length - barsupfront - 2):

valueOpenLow = 0

valueOpenHigh = 0

for i in range(1, barsupfront + 2):

value1 = open_[line + 1] - low[line + i]

value2 = open_[line + 1] - high[line + i]

valueOpenLow = max(value1, valueOpenLow)

valueOpenHigh = min(value2, valueOpenHigh)

if (valueOpenLow >= close[line + 1] * pipdiff_percentage) and (

-valueOpenHigh <= close[line + 1] * pipdiff_percentage / SLTPRatio):

trendcat[line] = 2 # -1 downtrend

break

elif (valueOpenLow <= close[line + 1] * pipdiff_percentage / SLTPRatio) and (

-valueOpenHigh >= close[line + 1] * pipdiff_percentage):

trendcat[line] = 1 # uptrend

break

else:

trendcat[line] = 0 # no clear trend

return trendcatThis code defines a function mytarget that attempts to identify potential trends and set target values accordingly. It calculates the difference between the open price and upcoming highs/lows within a specified timeframe (barsupfront). Based on these differences and thresholds defined by pipdiff_percentage and SLTPRatio, the function classifies the trend as uptrend, downtrend, or no clear trend. These classifications could then be used to set target buy/sell prices in a trading strategy.

Here’s the breakdown of the code provided:

The provided code defines a function mytarget that aims to set target values (presumably for buying and selling) based on a trend classification. Here's a breakdown of its functionality:

Parameters:

barsupfront(integer): The number of bars to look ahead from the current bar for trend classification.df1(pandas DataFrame): The DataFrame containing OHLC (Open, High, Low, Close) prices.

Function Logic:

- Initialization:

- It retrieves the length of the DataFrame (

length). - It extracts lists of high, low, close, and open prices (

high,low,close,open_). Note thatopenis renamed toopen_to avoid conflicts with Python's built-inopenfunction. - It initializes a list

trendcatwithlengthelements, all set toNone, which will eventually hold the trend category (uptrend, downtrend, or no trend) for each bar.

2. Trend Classification Loop:

- The code iterates through the DataFrame, starting from the

barsupfront-th bar to the second-last bar (length - barsupfront - 2). - Inside the loop:

- It calculates two values:

valueOpenLow: Maximum difference between the open price at the current bar and the low prices in the nextbarsupfront + 1bars.valueOpenHigh: Minimum difference between the open price at the current bar and the high prices in the nextbarsupfront + 1bars.- It checks these values against thresholds based on

pipdiff_percentage(a percentage of the asset's price) andSLTPRatio: - If

valueOpenLowis greater than or equal toclose[line + 1] * pipdiff_percentage(meaning the open is significantly lower than some of the upcoming lows) AND-valueOpenHighis less than or equal toclose[line + 1] * pipdiff_percentage / SLTPRatio(meaning the open is not significantly higher than some of the upcoming highs), it classifies the trend as downtrend (trendcat[line]is set to 2). - Conversely, if

valueOpenLowis less than or equal toclose[line + 1] * pipdiff_percentage / SLTPRatio(meaning the open is significantly higher than some of the upcoming lows) AND-valueOpenHighis greater than or equal toclose[line + 1] * pipdiff_percentage(meaning the open is not significantly lower than some of the upcoming highs), it classifies the trend as uptrend (trendcat[line]is set to 1). - If neither condition is met, it marks no clear trend (

trendcat[line]remains0).

3. Return:

- The function returns the

trendcatlist containing the trend classification for each bar (except the firstbarsupfrontbars). - pen_spark

#!!! pitfall one category high frequency

df['Target'] = mytarget(2, df)

df['Target'] = df['Target'].shift(1)

#df.tail(20)

df.replace([np.inf, -np.inf], np.nan, inplace=True)

df.dropna(axis=0, inplace=True)

# Convert columns to integer type

df = df.astype(int)

#df['Target'] = df['Target'].astype(int)

df['Target'].hist()

count_of_twos_target = df['Target'].value_counts().get(2, 0)

count_of_zeros_target = df['Target'].value_counts().get(0, 0)

count_of_ones_target = df['Target'].value_counts().get(1, 0)

percent_of_zeros_over_ones_and_twos = (100 - (count_of_zeros_target/ (count_of_zeros_target + count_of_ones_target + count_of_twos_target))*100)

print(f' count_of_zeros = {count_of_zeros_target}\n count_of_twos_target = {count_of_twos_target}\n count_of_ones_target={count_of_ones_target}\n percent_of_zeros_over_ones_and_twos = {round(percent_of_zeros_over_ones_and_twos,2)}%')

After assigning trend classifications (Target) based on the mytarget function, the code performs data cleaning by handling infinities and removing rows with missing values. It then analyzes the distribution of target values using a histogram and calculates the proportion of bars classified as each trend category. This helps assess the balance between clear uptrends, downtrends, and periods with no clear trend in the data.

1. Assigning Target Values and Shifting:

- The code assigns the output of

mytarget(2, df)(presumably trend classifications) to the'Target'column (df['Target'] = mytarget(2, df)). - It then shifts the

'Target'values by one position upwards (df['Target'] = df['Target'].shift(1)) because the trend classification is based on future price movements. This means the target value for barnis based on the trend classification for barn-1.

2. Handling Infinities and Missing Values:

- The code replaces positive and negative infinity (

np.infand-np.inf) withNaN(Not a Number) values in the DataFrame (df.replace([np.inf, -np.inf], np.nan, inplace=True)). This is necessary because some mathematical operations cannot handle infinities. - It then removes rows with missing values (

NaN) from the DataFrame (df.dropna(axis=0, inplace=True)) to ensure clean data for further analysis.

3. Converting Data Types (Commented Out):

- The line

df = df.astype(int)is commented out. This line would attempt to convert all columns in the DataFrame to integers. However, since the'Target'column likely contains categorical values (1, 2, or 0), converting it to integer might not be meaningful. You'd typically only convert numerical columns to integers if necessary for calculations.

4. Analyzing Target Distribution:

- The code plots a histogram of the

'Target'column (df['Target'].hist()). This helps visualize the distribution of target values (uptrend, downtrend, or no trend) across the data. - It then calculates the counts of each target value (1, 2, and 0) using

value_counts(). - Finally, it calculates the percentage of bars classified as “no trend” relative to the sum of bars classified as uptrend and downtrend (

percent_of_zeros_over_ones_and_twos). This provides insights into the balance between clear trends and unclear trends in the data.

This code segment effectively calculates target categories based on predefined criteria and provides insights into the distribution of these categories within the dataset.

Checking if the above Code is Giving Best Possible Returns for the “Target” Data Created:

# Check for NaN values:

has_nan = df['Target'].isnull().values.any()

print("NaN values present:", has_nan)

# Check for infinite values:

has_inf = df['Target'].isin([np.inf, -np.inf]).values.any()

print("Infinite values present:", has_inf)

# Count the number of NaN and infinite values:

nan_count = df['Target'].isnull().sum()

inf_count = (df['Target'] == np.inf).sum() + (df['Target'] == -np.inf).sum()

print("Number of NaN values:", nan_count)

print("Number of infinite values:", inf_count)

# Get the indices of NaN and infinite values:

nan_indices = df['Target'].index[df['Target'].isnull()]

inf_indices = df['Target'].index[df['Target'].isin([np.inf, -np.inf])]

print("Indices of NaN values:", nan_indices)

df['Target']

df = df.reset_index(inplace=False)

df['Date'] = pd.to_datetime(df['Date'])

df.set_index('Date', inplace=True)

def SIGNAL(df):

return df['Target']

from backtesting import Strategy

class MyCandlesStrat(Strategy):

def init(self):

super().init()

self.signal1 = self.I(SIGNAL, self.data)

def next(self):

super().next()

if self.signal1 == 1:

sl_pct = 0.025 # 2.5% stop-loss

tp_pct = 0.025 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 - sl_pct)

tp_price = self.data.Close[-1] * (1 + tp_pct)

self.buy(sl=sl_price, tp=tp_price)

elif self.signal1 == 2:

sl_pct = 0.025 # 2.5% stop-loss

tp_pct = 0.025 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 + sl_pct)

tp_price = self.data.Close[-1] * (1 - tp_pct)

self.sell(sl=sl_price, tp=tp_price)

bt = Backtest(df, MyCandlesStrat, cash=100000, commission=.001, exclusive_orders = True)

stat = bt.run()

stat

- Checking for Missing and Infinite Values:

- The code checks for the presence of

NaN(Not a Number) and infinite values in the'Target'column (df['Target']). - It then counts the number of occurrences and retrieves the indices of these values.

- These checks are crucial because backtesting libraries typically cannot handle missing or infinite values in signals.

2. Backtesting Framework Setup:

- The code defines a function

SIGNAL(df)that simply returns the'Target'column values. This function essentially provides the buy/sell signals based on the target classifications (1 for uptrend buy, 2 for downtrend sell). - It imports the

Strategyclass from thebacktestinglibrary. - It defines a custom strategy class

MyCandlesStratthat inherits fromStrategy. - The

initmethod initializes an indicator namedsignal1that holds the target values using theIfunction (presumably frombacktesting). - The

nextmethod defines the trading logic: - If the

signal1is 1 (uptrend), it places a buy order with a stop-loss and take-profit based on percentages of the closing price. - If the

signal1is 2 (downtrend), it places a sell order with a stop-loss and take-profit based on percentages of the closing price.

3. Backtesting and Evaluation:

- The code creates a

Backtestobject using thebacktestinglibrary. It provides the DataFrame (df), the strategy class (MyCandlesStrat), initial capital (cash), commission rate (commission), and setsexclusive_orderstoTrue(potentially to prevent overlapping orders). - It runs the backtest using the

bt.run()method and stores the results in thestatvariable.

Does this code definitively determine the effectiveness of the target values?

No, this code doesn’t definitively determine the effectiveness of the target values. Here’s why:

- Parameter Optimization: The stop-loss and take-profit percentages (

sl_pctandtp_pct) are fixed in the code. Optimizing these parameters for the specific strategy and market conditions could potentially improve performance. - Single Backtest Run: Running the backtest only once doesn’t account for the inherent randomness in financial markets. Ideally, you’d run the backtest multiple times with different random seeds to assess its robustness.

How to improve the code for target evaluation?

- Calculate Performance Metrics: Modify the code to calculate and print relevant performance metrics like Sharpe Ratio, drawdown, and total profit after the backtest run.

- Optimize Stop-Loss and Take-Profit: Implement a parameter optimization process to find the best stop-loss and take-profit values for the strategy using the target signals.

- Multiple Backtest Runs: Run the backtest with different random seeds (e.g., using a loop) and analyze the distribution of performance metrics to assess the strategy’s consistency.

By incorporating these improvements, wecan gain a more comprehensive understanding of how well the target values from the mytarget function perform in a backtesting framework. Remember, backtesting results are not guarantees of future performance, so real-world testing with a smaller capital allocation is essential before deploying a strategy with real money.

Scaling and splitting the dataframe for training and testing:

scaler = MinMaxScaler(feature_range=(0,1))

df_model = df.copy()

# Split into Learning (X) and Target (y) Data

X = df_model.iloc[:, : -1]

y = df_model.iloc[:, -1]

X_scaled = scaler.fit_transform(X)

# Define a function to reshape the data

def reshape_data(data, time_steps):

samples = len(data) - time_steps + 1

reshaped_data = np.zeros((samples, time_steps, data.shape[1]))

for i in range(samples):

reshaped_data[i] = data[i:i + time_steps]

return reshaped_data

# Reshape the scaled X data

time_steps = 1 # Adjust the number of time steps as needed

X_reshaped = reshape_data(X_scaled, time_steps)

# Now X_reshaped has the desired three-dimensional shape: (samples, time_steps, features)

# Each sample contains scaled data for a specific time window

# Align y with X_reshaped by discarding excess target values

y_aligned = y[time_steps - 1:] # Discard the first (time_steps - 1) target values

X = X_reshaped

y = y_aligned

print(len(X),len(y))

# Split data into train and test sets (considering time series data)

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.3, shuffle=False)1. Data Preparation:

- Copying Data: It creates a copy of the original DataFrame (

df_model = df.copy()) to avoid modifying the original data.

2. Splitting Features and Target:

- Separating Features (X) and Target (y): It separates the features (all columns except the last) and the target variable (the last column) using slicing (

X = df_model.iloc[:, : -1],y = df_model.iloc[:, -1]).

3. Scaling Features:

- MinMaxScaler: It creates a

MinMaxScalerobject to scale the features between 0 and 1 (scaler = MinMaxScaler(feature_range=(0,1))). This can be helpful for some machine learning algorithms that work better with normalized data. - Scaling X: It scales the feature data (

X) using thefit_transformmethod of the scaler (X_scaled = scaler.fit_transform(X)).

4. Reshaping Data (Windowing):

- Reshape Function: It defines a function

reshape_datathat takes the data and the number of time steps (time_steps) as input. - This function iterates through the data with a sliding window of

time_stepsand creates a new 3D array (reshaped_data). - Each element in the new array represents a sample, containing a sequence of

time_stepsdata points for each feature. - Reshaping Scaled X: It defines the number of time steps (

time_steps) and reshapes the scaled feature data (X_scaled) using thereshape_datafunction (X_reshaped = reshape_data(X_scaled, time_steps)). - This step transforms the data into a format suitable for time series forecasting models that require sequences of past observations to predict future values.

5. Aligning Target with Reshaped Data:

- Discarding Excess Target Values: Since the reshaped data (

X_reshaped) considers a window oftime_steps, the corresponding target values need an adjustment. It discards the firsttime_steps - 1target values fromyto align with the reshaped data (y_aligned = y[time_steps - 1:]).

6. Final Splitting (Train-Test):

- Train-Test Split: It splits the reshaped features (

X) and aligned target (y) into training and testing sets usingtrain_test_splitfrom scikit-learn (X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.3, shuffle=False)). - It sets

test_size=0.3to allocate 30% of the data for testing andshuffle=Falsebecause shuffling data in time series can disrupt the temporal order.

Overall, this code effectively addresses key aspects of data preparation for time series forecasting models:

- Scaling features to a common range can improve model performance for some algorithms.

- Reshaping data into a 3D structure with time steps allows models to learn from sequences of past observations.

- Aligning the target variable with the reshaped data ensures the model predicts for the correct time steps.

- Splitting data into training and testing sets with

shuffle=Falsepreserves the temporal order for time series forecasting.

Additional Considerations:

- The choice of scaler (MinMaxScaler, StandardScaler, etc.) might depend on the specific model and data characteristics.

- You might explore different window sizes (

time_steps) to see how they affect model performance. - Techniques like stationarity checks and differencing might be necessary for certain time series data before applying these steps.

2D CNN Model Manual Optimization

from sklearn.utils.class_weight import compute_class_weight

from keras import backend as K

def build_model(hp):

inputs = Input(shape=(X_train.shape[1], X_train.shape[2], 1))

x = Conv2D(hp.Int('conv_units', min_value=16, max_value=64, step=16), (5, 5), padding='same', activation='relu')(inputs)

x = MaxPooling2D(pool_size=(2, 2), padding='same')(x)

x = Dense(units=hp.Int('dense_units', min_value=100, max_value=300, step=50), activation='relu')(x)

x = Dropout(hp.Float('dropout_rate', min_value=0.1, max_value=0.5, step=0.1))(x)

x = Flatten()(x)

x = Dense(units=hp.Int('dense_units', min_value=100, max_value=300, step=50), activation='relu')(x)

outputs = Dense(3, activation='softmax')(x)

model = Model(inputs=inputs, outputs=outputs)

optimizer = Adam(learning_rate=hp.Choice('learning_rate', values=[1e-2, 1e-3, 1e-4]))

model.compile(optimizer=optimizer, loss='categorical_crossentropy', metrics=['accuracy', Precision(), Recall()])

return model

tuner = kt.Hyperband(

build_model,

objective=kt.Objective("val_recall", direction="max"),

max_epochs=20,

factor=3,

directory='my_dir',

project_name='hyperopt_cnn'

)

tuner.search(X_train, y_train_one_hot, epochs=10, validation_split=0.2)

# Get the best hyperparameters

best_hps = tuner.get_best_hyperparameters(num_trials=1)[0]

# Calculate class weights to handle class imbalance

class_weights = compute_class_weight('balanced', classes=np.unique(y_train), y=y_train)

class_weight_dict = dict(enumerate(class_weights))

# Build the model with the best hyperparameters

best_cnn_model = tuner.hypermodel.build(best_hps)

# Fit the model to the training data with best hyperparameters

# best_cnn_model.fit(X_train, y_train_one_hot, epochs=100, batch_size=24, validation_split=0.2, verbose=1, class_weight=class_weight_dict)

best_cnn_model.fit(X_train, y_train_one_hot, epochs=100, batch_size=18, validation_split=0.2, verbose=1)

This code defines and trains a 2D CNN-based model for classifying ETH price movements into three categories: neutral (0), long (1), and short (2). Here’s a breakdown:

Importing Libraries

from sklearn.utils.class_weight import compute_class_weight

from keras import backend as K

import keras_tuner as kt

from keras.models import Model

from keras.layers import Input, Conv2D, MaxPooling2D, Dense, Dropout, Flatten

from keras.optimizers import Adam

from keras.metrics import Precision, Recall

import numpy as np- compute_class_weight: Computes weights for classes to handle imbalanced datasets.

- keras.backend: Provides backend functions for operations.

- keras_tuner: Helps in hyperparameter tuning of models.

- Model: Used to create a Keras model.

- Layers: Various layers used to build the CNN model.

- Adam: The optimizer used to compile the model.

- Metrics: Precision and Recall metrics used to evaluate the model.

Building the Model

def build_model(hp):

inputs = Input(shape=(X_train.shape[1], X_train.shape[2], 1))

x = Conv2D(hp.Int('conv_units', min_value=16, max_value=64, step=16), (5, 5), padding='same', activation='relu')(inputs)

x = MaxPooling2D(pool_size=(2, 2), padding='same')(x)

x = Dense(units=hp.Int('dense_units', min_value=100, max_value=300, step=50), activation='relu')(x)

x = Dropout(hp.Float('dropout_rate', min_value=0.1, max_value=0.5, step=0.1))(x)

x = Flatten()(x)

x = Dense(units=hp.Int('dense_units', min_value=100, max_value=300, step=50), activation='relu')(x)

outputs = Dense(3, activation='softmax')(x)

model = Model(inputs=inputs, outputs=outputs)

optimizer = Adam(learning_rate=hp.Choice('learning_rate', values=[1e-2, 1e-3, 1e-4]))

model.compile(optimizer=optimizer, loss='categorical_crossentropy', metrics=['accuracy', Precision(), Recall()])

return model- inputs: Input layer accepting data with shape

(number_of_timesteps, number_of_features, 1). - Conv2D: Convolutional layer with filters determined by hyperparameters (

hp.Int). It extracts local patterns. - MaxPooling2D: Pooling layer to reduce the spatial dimensions.

- Dense: Fully connected layers to interpret the extracted features.

- Dropout: Regularization technique to prevent overfitting.

- Flatten: Converts the 2D matrix to a 1D vector for the dense layers.

- outputs: Final output layer with a softmax activation function for multi-class classification.

Hyperparameter Tuning

tuner = kt.Hyperband(

build_model,

objective=kt.Objective("val_recall", direction="max"),

max_epochs=20,

factor=3,

directory='my_dir',

project_name='hyperopt_cnn'

)- Hyperband: A Keras Tuner algorithm for hyperparameter tuning.

- objective: The metric to optimize during tuning (validation recall in this case).

- max_epochs: Maximum number of epochs to train.

- factor: Reduction factor for early stopping.

- directory/project_name: Where to save the tuning results.

Running the Tuner

tuner.search(X_train, y_train_one_hot, epochs=10, validation_split=0.2)- search: Runs the hyperparameter tuning process on the training data.

Get Best Hyperparameters

best_hps = tuner.get_best_hyperparameters(num_trials=1)[0]- Retrieves the best hyperparameters identified during tuning.

Compute Class Weights

class_weights = compute_class_weight('balanced', classes=np.unique(y_train), y=y_train)

class_weight_dict = dict(enumerate(class_weights))- compute_class_weight: Balances the classes by computing weights inversely proportional to their frequencies.

- class_weight_dict: Dictionary of class weights.

Build and Train the Model with Best Hyperparameters

best_cnn_model = tuner.hypermodel.build(best_hps)

best_cnn_model.fit(X_train, y_train_one_hot, epochs=100, batch_size=18, validation_split=0.2, verbose=1)- build: Builds the model with the best hyperparameters.

- fit: Trains the model on the training data.

Why 2D CNN Might be Better than 1D CNN for This Task

Feature Interactions:

- 2D CNN: Can capture interactions between different features over time. This is crucial for time series data with multiple features, as it can learn complex patterns.

- 1D CNN: Typically captures temporal patterns within a single feature or one-dimensional sequence of data.

Spatial Relationships:

- 2D CNN: More effective in understanding spatial relationships between features, which can be valuable when multiple related features are present.

- 1D CNN: Focuses on one-dimensional sequences, which may not capture interactions between multiple features as effectively.

Dimensionality Reduction:

- 2D CNN: Pooling layers can reduce the dimensions more efficiently by considering spatial context, leading to better generalization.

- 1D CNN: May require more layers or parameters to achieve similar dimensionality reduction, potentially increasing complexity.

Pattern Recognition:

- 2D CNN: Can detect complex patterns by applying filters across two dimensions (time and features), which is beneficial for multi-feature time series data.

- 1D CNN: Limited to recognizing patterns in one dimension, which may not be sufficient for complex multi-feature datasets.

Conclusion

The given code sets up a 2D CNN model with hyperparameter tuning using Keras Tuner. The model is designed to handle multi-class classification for time series data of cryptocurrencies. By leveraging 2D CNNs, the model can capture intricate patterns across both time and features, potentially leading to more accurate and robust predictions compared to 1D CNNs. The use of hyperparameter tuning ensures that the model is optimized for the given task, further enhancing its performance.

Additional Notes:

- The provided code might require adjustments based on your specific data and desired performance. Hyperparameter tuning (e.g., number of units, dropout rate, learning rate) is crucial for optimizing the model.

- Consider using techniques like normalization or standardization for your features to improve model performance.

Further Exploration:

- Experiment with different hyperparameters (number of layers, units, attention heads) to find the best configuration for your data and task.

- Consider incorporating additional features like technical indicators or fundamental data points to potentially improve the model’s prediction accuracy.

- Evaluate the model’s performance using various metrics like precision, recall, F1-score, or a custom metric based on your specific trading strategy.

Real-World Considerations:

- Financial markets are complex and influenced by various factors. Past price movements don’t guarantee future performance.

- Use the model predictions as a guide, not a definitive signal. Consider risk management strategies and other factors before making trading decisions.

- Backtest your model on historical data to assess its performance in different market conditions.

import numpy as np

import matplotlib.pyplot as plt

from sklearn.metrics import classification_report, confusion_matrix

import seaborn as sns

# # Reshape X_train and X_test back to their original shapes

# X_train_original_shape = X_train.reshape(X_train.shape[0], -1)

# X_test_original_shape = X_test.reshape(X_test.shape[0], -1)

# X_test_reshaped = X_test_original_shape.reshape(-1, 1, X_test_original_shape.shape[1])

# Now X_train_original_shape and X_test_original_shape have their original shapes

# Perform prediction on the original shape data

# y_pred = model.predict(X_test_reshaped)

y_pred = best_cnn_model.predict(X_test)

# Perform any necessary post-processing on y_pred if needed

# For example, if your model outputs probabilities, you might convert them to class labels using argmax:

y_pred_classes = np.argmax(y_pred, axis=1)

# Convert one-hot encoded y_test to class labels

y_test_classes = y_test

# Plot confusion matrix for test data

conf_matrix_test = confusion_matrix(y_test_classes, y_pred_classes)

# Plot confusion matrix

plt.figure(figsize=(8, 6))

sns.heatmap(conf_matrix_test, annot=True, cmap='Blues', fmt='g', cbar=False)

plt.xlabel('Predicted labels')

plt.ylabel('True labels')

plt.title('Confusion Matrix - Test Data')

plt.show()

# Compute classification report

report = classification_report(y_test_classes, y_pred_classes)

print("Classification Report:\n", report)

print("Confusion Matrix for Hyperopt Model:")

print(confusion_matrix(y_test_classes, y_pred_classes))

1. Imports:

confusion_matrixfromsklearn.metricsfor calculating the confusion matrix.matplotlib.pyplot(plt) andseaborn(sns) for creating the confusion matrix visualization.classification_reportfromsklearn.metricsfor generating a classification report.

2. Reshaping Data (Commented Out):

- The commented section addresses potential reshaping issues. It’s important to ensure your test data (

X_test) has the correct shape expected by the model for prediction.

3. Prediction:

y_pred = model_cnn.predict(X_test)performs predictions on the test data using your trained model.

4. Post-processing Predictions:

y_pred_classes = np.argmax(y_pred, axis=2)assumes your model outputs probabilities for each class (neutral, long, short). This line converts the probabilities to class labels by usingargmax(finding the index of the maximum value) along axis 2.

5. Converting True Labels:

y_test_classes = y_testassumes youry_testdata already contains class labels (0, 1, 2) for the test set.

6. Confusion Matrix:

conf_matrix_test = confusion_matrix(y_test_classes, y_pred_classes)calculates the confusion matrix for the test data. It shows how many samples from each true class were predicted into each class by the model.

7. Visualization:

- The code creates a heatmap visualization of the confusion matrix using

seaborn. This allows you to visually inspect how well the model classified each class. Ideally, you want to see high values on the diagonal, indicating correct classifications.

8. Classification Report:

class_report = classification_report(y_test, y_pred_classes)generates a classification report for the test data. This report provides metrics like precision, recall, F1-score, and support for each class, offering a more detailed breakdown of the model's performance.- pen_spark

Backtest with Test and Whole Data:

df_ens_test = df.copy()

df_ens = df_ens_test[len(X_train):]

df_ens['best_cnn_model_scaled'] = np.argmax(best_cnn_model.predict(X_test), axis=1)

df_ens['bcns'] = df_ens['best_cnn_model_scaled'].shift(1).dropna().astype(int)

df_ens = df_ens.dropna()

df_ens['bcns']

# df_ens = df.copy()

# # df_ens = df_ens_test[len(X_train):]

# df_ens['best_cnn_model_scaled'] = np.argmax(best_cnn_model.predict(X), axis=1)

# df_ens['bcns'] = df_ens['best_cnn_model_scaled'].shift(-1).dropna().astype(int)

# df_ens = df_ens.dropna()

# df_ens['bcns']

df_ens = df_ens.reset_index(inplace=False)

df_ens['Date'] = pd.to_datetime(df_ens['Date'])

df_ens.set_index('Date', inplace=True)

def SIGNAL_2_6(df_ens):

return df_ens['bcns']

class MyCandlesStrat_2_6(Strategy):

def init(self):

super().init()

self.signal1_1 = self.I(SIGNAL_2_6, self.data)

def next(self):

super().next()

if self.signal1_1 == 1:

sl_pct = 0.055 # 10% stop-loss

tp_pct = 0.055 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 - sl_pct)

tp_price = self.data.Close[-1] * (1 + tp_pct)

self.buy(sl=sl_price, tp=tp_price)

elif self.signal1_1 == 2:

sl_pct = 0.055 # 10% stop-loss

tp_pct = 0.055 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 + sl_pct)

tp_price = self.data.Close[-1] * (1 - tp_pct)

self.sell(sl=sl_price, tp=tp_price)

bt_2_6 = Backtest(df_ens, MyCandlesStrat_2_6, cash=100000, commission=.001)

stat_2_6 = bt_2_6.run()

stat_2_6

Youtube Link Explanation of VishvaAlgo v4.x Features — Link

get entire code and profitable algos @ https://patreon.com/pppicasso

Data Preparation

df_ens_test = df.copy()

df_ens = df_ens_test[len(X_train):]

df_ens['best_cnn_model_scaled'] = np.argmax(best_cnn_model.predict(X_test), axis=1)

df_ens['bcns'] = df_ens['best_cnn_model_scaled'].shift(1).dropna().astype(int)

df_ens = df_ens.dropna()- df_ens_test = df.copy(): Creates a copy of the original dataframe

dfto ensure the original data is not altered. - df_ens = df_ens_test[len(X_train):]: Selects the portion of the dataframe corresponding to the test set by slicing off the length of the training data.

- df_ens[‘best_cnn_model_scaled’] = np.argmax(best_cnn_model.predict(X_test), axis=1): Uses the trained CNN model to predict class labels on the test set (

X_test). Thenp.argmaxfunction is used to get the class with the highest probability for each prediction. - df_ens[‘bcns’] = df_ens[‘best_cnn_model_scaled’].shift(1).dropna().astype(int): Shifts the predicted class labels by 1 position to avoid look-ahead bias (using future data to make predictions for the current step). Drops any resulting

NaNvalues and converts the series to integers. - df_ens = df_ens.dropna(): Ensures no

NaNvalues are left in the dataframe.

Indexing and Date Formatting

df_ens = df_ens.reset_index(inplace=False)

df_ens['Date'] = pd.to_datetime(df_ens['Date'])

df_ens.set_index('Date', inplace=True)- df_ens = df_ens.reset_index(inplace=False): Resets the index of the dataframe without modifying it in place.

- df_ens[‘Date’] = pd.to_datetime(df_ens[‘Date’]): Converts the ‘Date’ column to datetime format.

- df_ens.set_index(‘Date’, inplace=True): Sets the ‘Date’ column as the index of the dataframe.

Signal Function

def SIGNAL_2_6(df_ens):

return df_ens['bcns']- SIGNAL_2_6(df_ens): A function that returns the ‘bcns’ column, which contains the shifted class labels (signals).

Custom Trading Strategy

class MyCandlesStrat_2_6(Strategy):

def init(self):

super().init()

self.signal1_1 = self.I(SIGNAL_2_6, self.data)

def next(self):

super().next()

if self.signal1_1 == 1:

sl_pct = 0.055 # 5.5% stop-loss

tp_pct = 0.055 # 5.5% take-profit

sl_price = self.data.Close[-1] * (1 - sl_pct)

tp_price = self.data.Close[-1] * (1 + tp_pct)

self.buy(sl=sl_price, tp=tp_price)

elif self.signal1_1 == 2:

sl_pct = 0.055 # 5.5% stop-loss

tp_pct = 0.055 # 5.5% take-profit

sl_price = self.data.Close[-1] * (1 + sl_pct)

tp_price = self.data.Close[-1] * (1 - tp_pct)

self.sell(sl=sl_price, tp=tp_price)- class MyCandlesStrat_2_6(Strategy): Defines a custom trading strategy class inheriting from

Strategy. - def init(self): Initialization method. The

self.signal1_1attribute is set to the signal functionSIGNAL_2_6, which provides the trading signals. - def next(self): The core logic of the strategy executed at each step.

- if self.signal1_1 == 1: If the signal is 1, a long position is taken with a 5.5% stop-loss and take-profit.

- elif self.signal1_1 == 2: If the signal is 2, a short position is taken with a 5.5% stop-loss and take-profit.

Backtesting the Strategy

bt_2_6 = Backtest(df_ens, MyCandlesStrat_2_6, cash=100000, commission=.001)

stat_2_6 = bt_2_6.run()

stat_2_6- bt_2_6 = Backtest(df_ens, MyCandlesStrat_2_6, cash=100000, commission=.001): Initializes a backtest with the prepared dataframe

df_ens, the custom strategyMyCandlesStrat_2_6, an initial cash balance of 100,000 units, and a commission rate of 0.1%. - stat_2_6 = bt_2_6.run(): Runs the backtest.

- stat_2_6: Outputs the results and statistics of the backtest.

Advantages of 2D CNN Over 1D CNN

Capturing Complex Patterns:

- 2D CNN: Can capture spatial relationships and interactions between different features across time, which is essential for multivariate time series data.

- 1D CNN: Typically focuses on temporal patterns within a single feature or one-dimensional sequence.

Dimensionality Reduction:

- 2D CNN: Efficiently reduces dimensionality while preserving important features through pooling layers.

- 1D CNN: May require more layers or parameters to achieve similar results.

Feature Interactions:

- 2D CNN: Can learn complex interactions between different features, providing a richer representation of the data.

- 1D CNN: Limited to learning patterns in one dimension, which may not capture the full complexity of multivariate data.

By using a 2D CNN, this approach leverages its ability to capture intricate patterns and interactions in multivariate time series data, potentially leading to better performance in predicting trading signals.

from keras.models import save_model

best_cnn_model.save(f"./models/best_cnn_model_2d_15m_ETH_SL55_TP55_ShRa_{round(stat_2_6['Sharpe Ratio'],2)}_time_{time.strftime('%Y%m%d%H%M%S')}.keras")Explanation:

- Import:

save_modelfromkeras.modelsis used to save the model.

2. Filename Definition:

- The filename is constructed using an f-string (formatted string literal). It incorporates various details:

- Path:

./models/: This specifies the directory where you want to save the model. - Model Name:

transformer_model: Base name for the model. - Hyperparameters:

_55sl_55tp: Likely indicates the stop-loss (SL) and take-profit (TP) values used in your backtesting strategy. - Data Info:

_eth_15m: Possibly refers to the data being Ethereum (ETH) prices with a 15-minute time frame. - Date:

_may_13th: The date the model was trained (May 13th). - Performance Metric:

_ShRa_{round(stat_1['Sharpe Ratio'],2)}: Appends the Sharpe Ratio from the backtesting results (stat_1), rounded to two decimal places. - File Extension:

.keras: Standard extension for Keras models.

3. Saving the Model:

save_model(model_transformer, filename): This line saves your trainedmodel_transformerto the specified file with the constructed filename.

Key Points:

- This approach provides a clear and informative way to save our model, including details about its training parameters, data, and performance.

- You can modify the filename structure to include additional information relevant to your needs.

Let’s Backtest entire data with saved model:

from keras.models import load_model

# # Load the ensemble_predict function using joblib

best_model = load_model('./models/cnn_model_2d_15m_ETH_May_16_SL55_TP55_ShRa_0.68_time_20240527170917.keras')Intended Functionality:

- Import:

load_modelfromkeras.modelsis used to load a saved model.

2. Loading the Model:

best_model = load_model('./models/transformer_model_55sl_55tp_eth_15m_may_13th_ShRa_0.78.keras'): This line attempts to load a model saved with the filenametransformer_model_55sl_55tp_eth_15m_may_13th_ShRa_0.78.kerasfrom the directory./models/.

df_ens = df.copy()

# df_ens = df_ens_test[:len(X)]

y_pred = best_model.predict(X)

# Perform any necessary post-processing on y_pred if needed

# For example, if your model outputs probabilities, you might convert them to class labels using argmax:

# y_pred_classes = np.argmax(y_pred, axis=1)

# y_pred = np.argmax(y_pred, axis=1) # for lstm, tcn, cnn models

y_pred = np.argmax(y_pred, axis=2) # for transformers model

df_ens['best_model'] = y_pred

df_ens['bm'] = df_ens['best_model'].shift(1).dropna().astype(int)

df_ens['ema_22'] = ta.EMA(df_ens['Close'], timeperiod=22)

df_ens['ema_55'] = ta.EMA(df_ens['Close'], timeperiod=55)

df_ens['ema_108'] = ta.EMA(df_ens['Close'], timeperiod=108)

df_ens = df_ens.dropna()

df_ens['bm']

df_ens = df_ens.reset_index(inplace=False)

df_ens['Date'] = pd.to_datetime(df_ens['Date'])

df_ens.set_index('Date', inplace=True)

def SIGNAL_010(df_ens):

return df_ens['bm']

def SIGNAL_0122(df_ens):

return df_ens['ema_22']

def SIGNAL_0155(df_ens):

return df_ens['ema_55']

def SIGNAL_01108(df_ens):

return df_ens['ema_108']

class MyCandlesStrat_010(Strategy):

def init(self):

super().init()

self.signal1_1 = self.I(SIGNAL_010, self.data)

self.ema_1_22 = self.I(SIGNAL_0122, self.data)

self.ema_1_55 = self.I(SIGNAL_0155, self.data)

self.ema_1_108 = self.I(SIGNAL_01108, self.data)

def next(self):

super().next()

# if (self.signal1_1 == 1) and (self.data.Close > self.ema_1_22) and (self.ema_1_22 > self.ema_1_55) and (self.ema_1_55 > self.ema_1_108):

# sl_pct = 0.025 # 10% stop-loss

# tp_pct = 0.025 # 2.5% take-profit

# sl_price = self.data.Close[-1] * (1 - sl_pct)

# tp_price = self.data.Close[-1] * (1 + tp_pct)

# self.buy(sl=sl_price, tp=tp_price)

# elif (self.signal1_1 == 2) and (self.data.Close < self.ema_1_22) and (self.ema_1_22 < self.ema_1_55) and (self.ema_1_55 < self.ema_1_108):

# sl_pct = 0.025 # 10% stop-loss

# tp_pct = 0.025 # 2.5% take-profit

# sl_price = self.data.Close[-1] * (1 + sl_pct)

# tp_price = self.data.Close[-1] * (1 - tp_pct)

# self.sell(sl=sl_price, tp=tp_price)

# def next(self):

# super().next()

# if (self.signal1_1 == 1) and (self.ema_1_22 > self.ema_1_55) and (self.ema_1_55 > self.ema_1_108):

# sl_pct = 0.025 # 10% stop-loss

# tp_pct = 0.025 # 2.5% take-profit

# sl_price = self.data.Close[-1] * (1 - sl_pct)

# tp_price = self.data.Close[-1] * (1 + tp_pct)

# self.buy(sl=sl_price, tp=tp_price)

# elif (self.signal1_1 == 2) and (self.ema_1_22 < self.ema_1_55) and (self.ema_1_55 < self.ema_1_108):

# sl_pct = 0.025 # 10% stop-loss

# tp_pct = 0.025 # 2.5% take-profit

# sl_price = self.data.Close[-1] * (1 + sl_pct)

# tp_price = self.data.Close[-1] * (1 - tp_pct)

# self.sell(sl=sl_price, tp=tp_price)

if (self.signal1_1 == 1):

sl_pct = 0.035 # 10% stop-loss

tp_pct = 0.025 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 - sl_pct)

tp_price = self.data.Close[-1] * (1 + tp_pct)

self.buy(sl=sl_price, tp=tp_price)

elif (self.signal1_1 == 2):

sl_pct = 0.035 # 10% stop-loss

tp_pct = 0.025 # 2.5% take-profit

sl_price = self.data.Close[-1] * (1 + sl_pct)

tp_price = self.data.Close[-1] * (1 - tp_pct)

self.sell(sl=sl_price, tp=tp_price)

bt_010 = Backtest(df_ens, MyCandlesStrat_010, cash=100000, commission=.001)

stat_010 = bt_010.run()

stat_010

Youtube Link Explanation of VishvaAlgo v4.x Features — Link

get entire code and profitable algos @ https://patreon.com/pppicasso

This code builds upon your previous strategy by incorporating a Transformer model prediction ('best_model') along with Exponential Moving Averages (EMAs) to generate buy and sell signals for a backtesting strategy. Here's a breakdown:

1. Data Preparation:

df_ens = df.copy(): Creates a copy of the original DataFrame (df).y_pred = best_model.predict(X): Makes predictions on the entire DataFrame (X) using your loaded Transformer model (best_model).df_ens['best_model'] = y_pred: Adds a new column'best_model'to the DataFrame containing the model predictions.df_ens['bm'] = df_ens['best_model'].shift(1).dropna().astype(int): Similar to before, this creates a shifted signal column'bm'based on the predicted labels, but here it might include predictions for the entire DataFrame.df_ens['ema_22'] = ta.EMA(df_ens['Close'], timeperiod=22): Calculates the 22-period EMA for the 'Close' price and adds it as a new column'ema_22'.df_ens['ema_55'] = ta.EMA(df_ens['Close'], timeperiod=55): Similar to above, calculates the 55-period EMA and adds it as'ema_55'.df_ens['ema_108'] = ta.EMA(df_ens['Close'], timeperiod=108): Calculates the 108-period EMA and adds it as'ema_108'.df_ens = df_ens.dropna(): Removes rows with missing values (likely the first row due to shifting).

2. Signal Functions (Outside the Code Block):

- These functions (

SIGNAL_010,SIGNAL_0122, etc.) simply return the corresponding columns from the DataFrame ('bm','ema_22', etc.) used for generating the signals.

3. Backtesting Strategy Class (MyCandlesStrat_010):

- Inherits from

Strategy. def init(self): Initializes indicators for the Transformer model predictions (self.signal1_1) and EMAs (self.ema_1_22, etc.).

4. Backtesting Logic (in next function):

- The commented-out section shows a more complex logic considering the relationship between the Transformer predictions and the EMAs for buy/sell decisions.

- The current active section uses a simpler approach:

- If

self.signal1_1(Transformer prediction) is 1 (long): - Buy with stop-loss (SL) at 3.5% below current close and take-profit (TP) at 2.5% above.

- If

self.signal1_1is 2 (short): - Sell with SL at 3.5% above current close and TP at 2.5% below.

5. Backtesting and Results:

bt_010 = Backtest(df_ens, MyCandlesStrat_010, cash=100000, commission=.001): Creates a backtest object using the DataFrame, strategy class, and other parameters.stat_010 = bt_010.run(): Runs the backtest and stores the results instat_010.stat_010: This variable likely contains the backtesting statistics you can analyze.

Key Points:

- This strategy combines predictions from our Transformer model with technical indicators (EMAs) for generating signals.

- You can experiment with different conditions in the

nextfunction to create more sophisticated trading strategies. - Remember that backtesting results may not guarantee future performance, and proper risk management is crucial for real-world trading

Conclusion for 2D CNN Model:

The given code sets up a 2D CNN model with hyperparameter tuning using Keras Tuner. The model is designed to handle multi-class classification for time series data of cryptocurrencies. By leveraging 2D CNNs, the model can capture intricate patterns across both time and features, potentially leading to more accurate and robust predictions compared to 1D CNNs. The use of hyperparameter tuning ensures that the model is optimized for the given task, further enhancing its performance.

Applying 2D CNN Model for Other Assets and Short List the Best:

From here on we will explain about how to use the same trained model to short list best assets after doing certain backtest on all the assets after downloading the data from tradingview for backtest

Importing Necessary packages and setting up Model & Exchange APi with CCXT

import time

import logging

import io

import contextlib

import glob

import ccxt

from datetime import datetime, timedelta, timezone

import keras

from keras.models import save_model, load_model

import numpy as np

import pandas as pd

import talib as ta

from sklearn.preprocessing import MinMaxScaler

import warnings

from threading import Thread, Event

import decimal

import joblib

from tcn import TCN

# from pandas.core.computation import PerformanceWarning

# Suppress PerformanceWarning

warnings.filterwarnings("ignore")

# NOTE: Train your own model from the other notebook I have shared and use the most successful trained model here.

# model_file_path = './model_lstm_1tp_1sl_2p5SlTp_April_5th_ShRa_1_49_15m.hdf5'

model_file_path = './models/transformer_model_55sl_55tp_eth_15m_may_13th_ShRa_0.78.keras'

model_name = model_file_path.split('/')[-1]

##################################### TO Load A Model #######################################

# NOTE: for LSTM based neural network model you can directly load_model with model_file_path as given below

# Load your pre-trained model, keras trained model will only take load_model from keras.models and not from joblib

model = load_model(model_file_path)

# # or

# model = tf.keras.models.load_model(model_file_path)

# NOTE: for TCN based neural network model, you need to add custom_objects while loading the model, it is given below

# # Define a dictionary to specify custom objects

# custom_objects = {'TCN': TCN}

# model = load_model(model_file_path, custom_objects = custom_objects)

##########################################################################################

########################## Adding the exchange information ##############################

exchange = ccxt.binanceusdm(

{

'enableRateLimit': True, # required by the Manual

# Add any other authentication parameters if needed

'rateLimit': 250, 'verbose': True

}

)

# NOTE: I used https://testnet.binancefuture.com/en/futures/BTCUSDT for testnet API (this has very bad liquidity issue for various assets and many other issues but can be used for purely testiug purpose)